Understanding Total Income, Taxable Income, Exemptions and Deductions

27 Feb, 2024

Share this Blog with your contacts

Have you ever wondered how taxes work? Don't worry; you're not alone! Taxes can seem like a big, scary monster, but with a little help, they're not so scary after all. Today, we're going to talk about some essential tax concepts: total income, taxable income, exemptions, and deductions. And guess what? We'll make it as easy as pie, so grab a snack and let's get started on our tax adventure!

What Is Total Income and Why Does It Matters?

What's Total Income?

So, total income is like a big basket that holds all the money you make in a year. It includes your salary if you have a job, any extra money you make from things like selling stuff, and even the interest you earn from your piggy bank savings!

Why Should You Care About Total Income?

Well, total income is super important because it's the starting point for figuring out how much tax you owe. Just like you need to know how much flour you have to bake a cake, the government needs to know how much money you make to calculate your taxes.

How Does Total Income Affect Your Taxes?

Let's say you make Rs. 50,000 in a year from your allowance, chores, and selling lemonade in the summer. That Rs. 50,000 is your total income. When it's tax time, the government uses this number to figure out how much tax you owe. If you make more money, you might have to pay more tax.

How Taxable Income Is Different From Total Income and Why It Matters?

What Makes Some Income Taxable?

Now, not all the money in your total income is taxable. Some of it gets special treatment, like when your grandpa gives you birthday money or your friend pays you back for that awesome slime you sold them. This money might not be taxable.

Why Do You Need to Know About Taxable Income?

Understanding taxable income is like knowing which candies are in your trick-or-treat bag – it helps you know what you have to share with the tax monster (the government). If you don't know what counts as taxable income, you might end up giving away more than you need to!

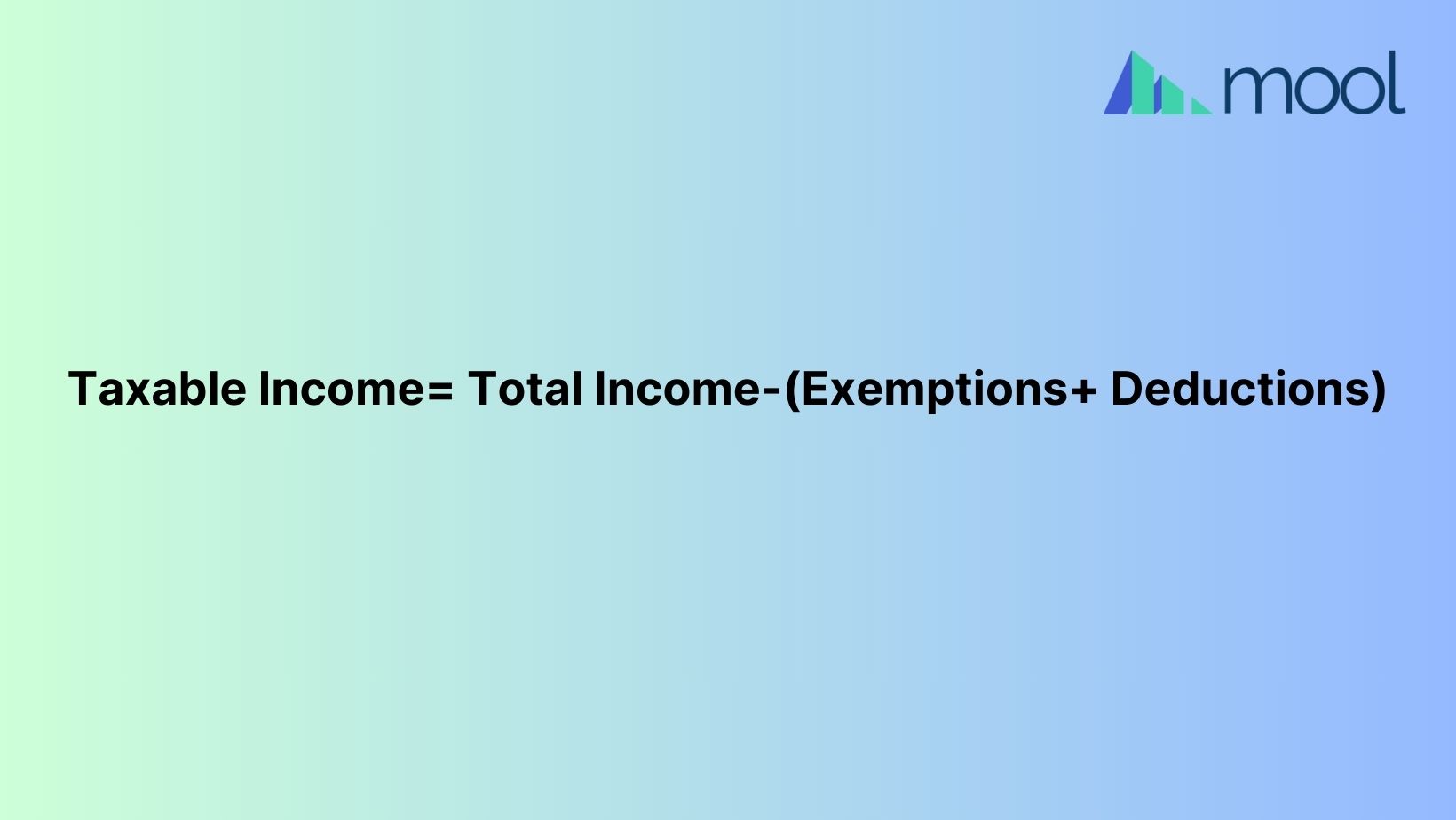

How Do You Figure Out Taxable Income?

To calculate your taxable income, you start with your total income and then subtract any exemptions and deductions. We'll talk about those in a bit, but for now, just remember that taxable income is what's left after you take away the tax-free stuff.

How to Use Exemptions to Lower Your Taxes?

What Are Exemptions?

Exemptions are like little magic spells that make some of your income disappear – in a good way! They're special rules that let you reduce your taxable income if you meet certain conditions. For example, if you have a big family, you might get an exemption for each family member.

Why Do Exemptions Exist?

The government gives out exemptions to help families with lots of kids or people with special needs. They understand that taking care of a big family or someone who needs extra help can cost a lot of money. So, exemptions are like a little pat on the back for doing a great job!

How Can Exemptions Save You Money?

Let's say you have two younger siblings, and each of them gives you an exemption of Rs. 10,000. That means Rs. 20,000 of your income magically disappears! So, if your total income was Rs. 100,000, after exemptions, it would be only Rs. 80,000 – and that means less tax for you to pay!

How to Lower Your Taxes with Deductions?

What's the Deal with Deductions?

Deductions are like secret codes that let you subtract certain expenses from your taxable income. They're things like money you spend on school books, medical bills, or even donations to charity. Deductions are super cool because they help you keep more of your money!\

Why Use Deductions?

Imagine you have a pizza, and someone takes a slice before you can even take a bite – not cool, right? Well, deductions are like making sure you get to eat the whole pizza! They help you keep more of your hard-earned money instead of giving it all to the tax monster.

How Do You Get Deductions?

To get deductions, you need to keep track of your expenses throughout the year. So, if you buy school supplies, keep the receipts! When it's tax time, you can use those receipts to lower your taxable income and pay less tax.

Important Income Tax Exemptions and Deductions Allowed to Salaried Individuals

Here are some common income tax exemptions and deductions available to the salaried class in India:

1. Standard Deduction: A fixed deduction allowed from the salary income of employees. As of now, it is set at ₹50,000.

2. House Rent Allowance (HRA): If you're paying rent for accommodation and receiving HRA from your employer, a portion of the HRA can be exempt from tax, subject to certain conditions. HRA calculator

3. Leave Travel Allowance (LTA): Expenses incurred on travel during leave can be exempt from tax, subject to specific rules and limits.

4. Employee Provident Fund (EPF): Contributions made towards EPF are eligible for deduction under Section 80C of the Income Tax Act.

5. National Pension System (NPS): Contributions to NPS are eligible for tax deduction under Section 80CCD(1) of the Income Tax Act. NPS calculator

6. Medical Allowance: Reimbursements received for medical expenses incurred by the employee or their family can be exempt from tax, subject to certain limits and conditions.

7. Children's Education Allowance: Expenses incurred on the education of children can be exempt from tax up to a certain limit.

8. Conveyance Allowance: Expenses incurred on commuting between the place of residence and the place of work can be exempt from tax up to a certain limit.

9. Medical Insurance Premium: Premium paid towards medical insurance for self, spouse, children, or parents is eligible for deduction under Section 80D of the Income Tax Act.

10. Interest on Home Loan: Interest paid on a home loan for a self-occupied property is eligible for deduction under Section 24(b) of the Income Tax Act, subject to certain conditions and limits. Home loan calculator

11. Education Loan Interest: Interest paid on education loans for higher studies is eligible for deduction under Section 80E of the Income Tax Act.

12. Deduction for Persons with Disabilities: Expenses incurred for the medical treatment, training, and rehabilitation of a disabled person can be claimed as a deduction under Section 80DD and Section 80U of the Income Tax Act.

13. Professional Tax: Professional tax paid by the employee to the state government is eligible for deduction from the total income.

14. Deduction for Donations: Donations made to specified charitable institutions and funds are eligible for deduction under Section 80G of the Income Tax Act.

15. Gratuity: Gratuity received by employees on retirement or resignation is exempt from tax up to a certain limit, based on the provisions of the Payment of Gratuity Act, 1972. Gratuity calculator

16. Transport Allowance: Allowance granted to meet the expenditure incurred on commuting between the place of residence and the place of work is eligible for exemption up to a certain limit.

These exemptions and deductions are subject to specific conditions, limits, and rules as per the Income Tax Act of India.

Conclusion

Congratulations, tax pros! You've made it through our tax adventure, and now you know all about total income, taxable income, exemptions, and deductions. Remember, while taxes might seem scary, they're not so bad when you know how they work. So, keep learning, keep asking questions, and don't forget to save those receipts! Happy tax time!

Access exclusive content and expert tips by subscribing to our newsletter today!

Follow us on

Mool is a leading financial startup that aims to create a sustainable solution for corporate employees by facilitating effective tax planning, smart investments, insurance, and borrowing options. Mool simplifies the personal financial and taxation jargon and makes it accessible to all. With the products of Mool, organizations and employees can now maximize the value of their salaries without a hassle. Mool’s mission is to create a platform to educate everyone, optimize the growth of their money, and empower them with rich facts and proven analysis for decision making.